Apple vs. Blackberry

Could you tell the difference before it's too late?

SUMMARY

I believe that its possible to improve our chances of investing in “disruptive” companies if we wait until its later in the cycle and the winners are more clearly identifiable vs trying to get in early and believe we can pick the winners from the hoards of future losers.

FOUR CLUES TO HELP US

1) Has a new taxonomy been established?

2) Has “massive disruption” downshifted to "incremental progress?”

3) Have major incumbents surrendered?

4) Has an event occurred that caused popular sentiment to diverge strongly from the trending business fundamentals?

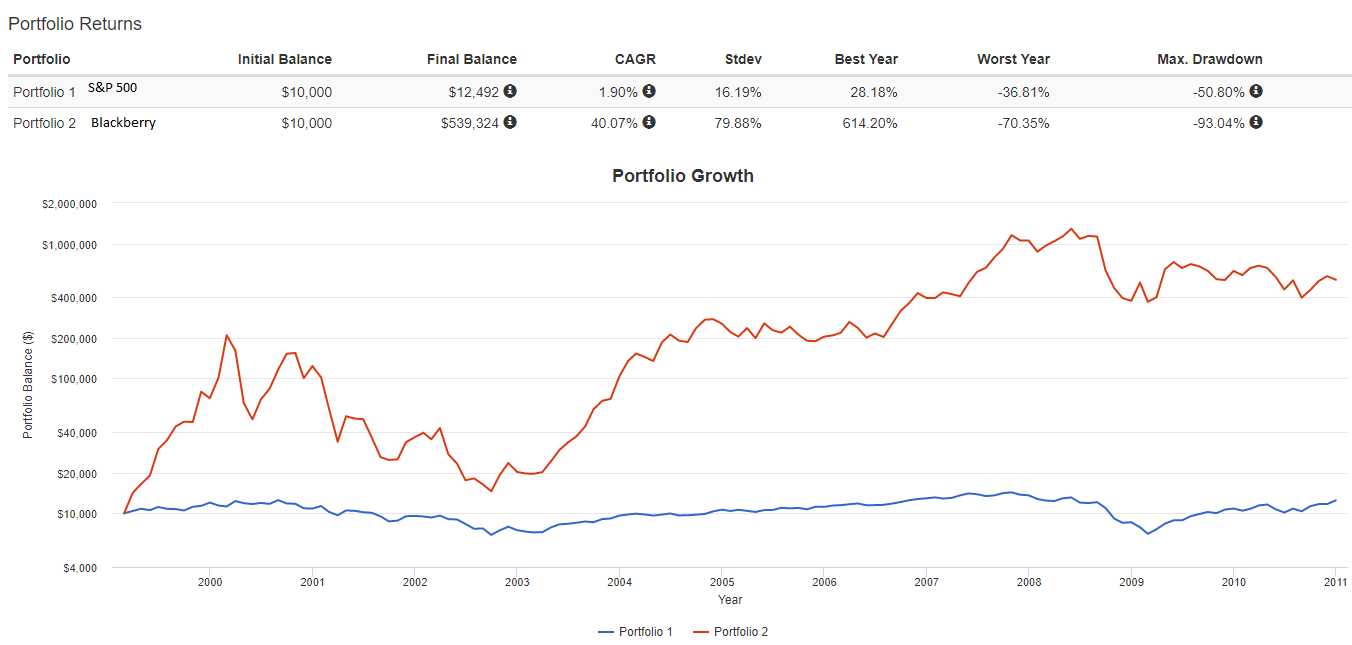

Apple has become one of the most successful investments in history.

A $10,000 investment in Apple the day the first iPhone was released (June, 2007) held till end of February 2020 is worth $325,000 for a compounded return of 28.8% vs the S&P $33,000; a 9% CAGR.

Furthermore, it was “obvious” at the time that the iPhone was something special. Apple had to limit the number of sales per user. Long lines formed early prior to its release. It was a worldwide object of admiration and envy. Apple sold 1 million phones in 3 months.

Yet how soon we forget.

Back in 1999 a company called Blackberry (Research in Motion) released its 850 - the world’s first email pager. Blackberry IPO’d shortly thereafter in the heady days of internet mania. Despite crashing with the rest of the tech market (2000-2002) by the beginning of 2010 (years after the first iPhone was released) $10,000 invested in Blackberry was worth $539,000 for a compounded rate of 40% (BB March 1999 - Dec 2010) - a staggering achievement when compared to the S&P’s CAGR of 1.9%.

But it was not to last.

By the end of the next decade, the $539,000 fortune would dwindle to $61,000 and the compounded rate would fall to 8.68%. Despite this collapse, 20 year shareholders STILL manage to outperform the S&Ps 7.17% annualized return providing $45,000 on the original $10,000 investment.

Ruin was visited most harshly on those who bought Blackberry near the peak - not in the .com bubble days; but eight years later in 2008. A $10,000 investment in Jan 2008 resulted in just $886 by February of 2021. Slightly diminished ruin would visit those who believed they were getting a bargain after the first substantial drop. Investors waiting a year (Jan 2009) could claim $2400 instead. Three times better, but little cheering was heard.

Apple, in contrast, has never suffered such a fall.

Between 1985 and the end of 2000 (post bubble popping) Apple shareholders had a 7.1% annual return. Not incredible, but not terrible. And even during the period when Jobs was gone (1985-1997); shareholders still received a 2% annual return - relatively terrible, but far better than a permanent loss of capital. By the end of 2005 those 1985 shareholders were back to incredible annualized returns of 17.5%; a fantastic payoff for just hanging on and doing nothing.

Even investors who bought Apple at the peak in March of 2000 were made whole by Oct of 2004 (albeit the 80% drop was not something most investors could stomach - but this was not unique to Apple during this time, Blackberry dropped 93%).

So one business is dominant early, stumbles, then recovers to become one of the greatest investments of all time. While another is dominant early, stumbles and never comes back (at least not yet).

If you thought Blackberry was Apple, you got crushed.

If you thought Apple was Blackberry, you missed out.

But why? And what clues can we use to help us improve our hit ratio?

Clue #1: THE LIFECYCLE OF DISRUPTION

To answer that question requires technological archeology and an appreciation for the dynamic nature of disruption.

While happening, rapid disruption feels like a terminal process (remember the 8th deadly sin - extrapolation). In reality, as the scale of new behaviors starts to be broadly adopted and solidify, the magnitude of change slows and substantial disruption gives way to incremental improvement - occasionally being reduced to mere cosmetic or stylistic improvements.

Consider this snippet from a Jan. 6th 1985 article in the Los Angeles Time:

“About 3,000 auto companies, many of them in people’s garages, have started and failed in this country. Now, we’re down to four U.S.-based car manufacturers. Meanwhile, we have about 500 computer companies and 4,000 software outfits, many of them still in people’s garages. A few years hence, everyone says, we’ll be down to a handful of computer makers.”

(High Tech: Auto Makers' History Revisited - Los Angeles Times (latimes.com)

Prescient.

While there are still a great number of software companies in the US, the number of PC manufacturers has reduced considerably with the top 3 dominating and the “other” category continuing to drop:

Investing in an auto manufacturer 100 years ago felt a lot like investing in a “disruptive technology” company does today. The TAM was almost unimaginably large as the horse would be ultimately replaced by far superior technology. EVERYONE could see that the automobile was obviously going to be huge. If you missed out and hitched your wagon to “old” businesses (banks, insurance, etc.) you were missing the future. What everyone could not see is WHICH automobile company would be huge and how “good” the automobile business would for investors be in the long run.

Investing in a PC manufacturer in the 1980s and 1990s had a similar feel. Computer companies were springing up everywhere: Commodore, Wang, Tandy, TI, Atari. Everyone had their killer machine and fortunes ebbed and flowed apace. Yet just a few decades later, it’s hard to imagine that Lenovo, Dell, HP and Apple will be unexpectedly and rapidly replaced by an upstart PC manufacturer. It’s possible, of course, but it seems more likely that the entire PC business gets disrupted - a risk that was and is still discussed as the power of smart phones, tablets, AR and VR devices keep progressing in power.

The other factor is market saturation and adoption speed. According to the Federal Highway Administration (which has data going back to 1900); in 1900 there were a total of 8000 registered automobiles. By 1905 it was nearly 80,000 (10x growth in 5 years). By 1912 it had increased by another order of magnitude to 800,000. Not slowing down, 1920 saw 8,000,000 registered vehicles. The 80,000,000 mark took another 5 decades (1967). Finally between 1980 and 1995 numbers stayed pretty steady at around 125,000,000.

When a market is increasing by an order of magnitude every few years, the opportunity for disruption is massive. Companies that dominated the market with 8,000 vehicles will get destroyed by ones that can focus on the 80,000 customers. Subsequently, those that scale to 8,000,000 or even 80,000,000 may be different businesses than those that make 80,000. Capitalism is brutal… and capitalism during rapid scaling is exponentially brutal.

Television had a similar growth curve and period of corporate innovation and collapse. Since 1939 there have been about 220 manufacturers that made sets in and/or for the US, of which only 23 still exist. In 1969 Admiral had been a TV manufacturer for 20 years, but 10 years later it would disappear. Indeed, the 60s and 70s were a very dangerous time to be a Television manufacturer, just as the 30s and 40s was tough on car makers.

This history is relevant to the discussion of Blackberry vs. Apple.

By the 1990s, Apple had already emerged as one of the few winners in the PC wars (albeit not a “top” winner by market share but rather a solid niche winner). Once in that position, Apple was able to maintain reasonable level of sales because of a dedicated user base and a more incremental disruption. Between the mid 1990s and today little has changed. While the power, usability and manufacture of the components has changed; our behaviors have stayed relatively static. We still use GUIs, have a 2 (or 3) button mouse, a QWERTY keyboard, storage and a monitor.

Clue 2: Taxonomy

We must also remember that the taxonomy of today is not the taxonomy of yesterday. The word “Personal Computer” does not enter into common vocabulary until well into the battle for dominance has commenced. Similarly, the wide use of the term “Smartphone” does not commonly appear until well into 2011 - at which point the battle for dominance is largely over (Blackberry sales started dropping in 2012).

This delay in taxonomy creates a distorted view of history. From our vantage point today (March 2020) we can clearly see the battle between the various families of devices and companies that were attempting to push them into the market. Palm, Blackberry, Motorola, Nokia - they can all be scoffed at from our all knowing vantage point. Blackberry’s adherence to a physical keyboard and focus on business users appears was an obvious strategic blunder committed by a blind, lazy, and stubborn management.

At the time, however, this was not so obvious. Post iPhone launch, Blackberry sales continued to grow and the media had many articles and interviews about how Apple’s appeal to the main stream consumer would never spill over into the business user. Its lack of basic functionality critical to business needs would prevent it from capturing the lucrative business user market.

Nor is this analysis without precedent. Apple’s PC strategy of a walled garden, high prices and obsession with “quality” proved to be a failed strategy against the army of “WinTel” clones that embraced a low coast, open ecosystem. Apple “Computer” was focusing on a few niche areas: education, art, publishing - but it never crossed into the business world nor did it achieve home dominance.

As is often the case with disruption, the past is not prologue and the strategies of yesterday may not provide a roadmap for for tomorrow.

Clue 3: Crying Uncle and Disruptive Iteration

During the 30s and 40s many auto manufacturers simply gave up and surrendered the battle field. Similarly, PC manufacturers including Commodore, Tandy, and Atari took their PC ball and went home. I would argue that this is where we are with smartphones today. Microsoft and Amazon have surrendered their attempts to enter the market and prior dominant players like Nokia and Blackberry have disappeared either voluntarily or involuntarily. I would be surprised if the list of dominant Smartphone manufacturers changes dramatically from what we have seen over the past few years. This, of course CAN happen, but we should be able to spot it easier than we could a few decades ago.

During the 90s and 2000s, mobile phones were going through incredibly rapid periods of disruption and adoption. A mobile phone in the early 90s looks and acts nothing like a Smartphone does today. In the late 80s phones were big and heavy and primarily used to make calls in emergency situations by limo riding business executives. By the mid 90s they were much more broadly distributed (but still relatively expensive) luxury goods - with pagers being a much more inexpensive alternative. Today, smart phones are portable computers used by most people on the planet. They are cameras, wallets, news reading devices, music players, movie players and so on. Making phone calls is one of the least used functions. When was the last time you saw a phone manufacturer tout it’s voice clarity as a major feature?

Yet in the past few years most of the “disruption” is bigger screen sizes, faster processors, higher pixel resolution, more storage and minor “improvements” like removing the headphone jack. Most people probably can’t tell which iPhone is the latest version and which is one or two generations behind. No one was confused between the iPhone 1 and the Blackberry.

When disruption gives way to incremental innovation, you can feel much more confident about the longevity of the winners.

How can this help us as investors?

Can we confidently choose today’s Apple and avoid today’s Blackberry? Not likely, but we an take a different approach.

What we can do is try and evaluate the relative maturity of the disruption cycle and then evaluate the value of the dominant business within it.

By the end of 2014 it was fairly obvious (or at least much more obvious) that Blackberry was dead and Apple was going to be one of the big winners. The disruption in Smartphones had also somewhat calmed down and we were entering the incremental cycle. Blackberry had fallen from 19B in revenue (2011) to 6B in revenue (2014). In contrast Apple had continued to grow from 100B to 182B in revenue (a similar pattern had played out with tablets where Apple also dominated and many other new companies surrendered the battlefield).

Despite revenue growth of 27% in the prior year, EBIT margins of almost 30% and FCF Yield of 11%, Apple’s EV/Revenue was at just 2x and it’s P/E was at 12x (end of 2015). Apple was priced as a fairly moderate “value” stock.

This may seem unusual, but it is not that uncommon.

Consider that at the end of 2018, Facebook was also the obvious winner (or as obvious as can be expected) in social media - having destroyed MySpace and caused Google to retreat from the battle field. It was trading at 6x EV/S and at a P/E of 17; despite 37% revenue growth and EBIT margins of over 40%.

At the end of 2011 - just one year after Blockbuster left the battlefield in bankruptcy, Netflix was priced at just 1.1x sales and a 16 P/E; despite nearly 50% revenue growth and EBIT margins on 12% (Note: this was exceptional. For most of its life Netflix had very high multiples, and until it had the scale to increase pricing valuations always appeared high - I submit it has to be valued differently, but that’s another topic). By the end of 2011, it was not that much of a stretch to believe that Netflix would continue to be a dominant player in streaming and that streaming was likely the future of video entertainment.

Clue #4: Wait for a stumble.

Why does this happen?

One key is to understand the difference between underlying business growth and market sentiment. Once a company establishes dominance and effectively eliminates the ability for competitors to easily enter the market; it is likely to maintain its inertia for some time. However, they are likely to make some mistakes along the way; causing investor and public sentiment to swing wildly. This can represent a great opportunity.

In the case of Netflix it was the business strategy to separate out the DVD rental business from the streaming business which temporarily angered customers (and sent some away). But the magnitude of the impact on the business was much less than the headlines claim. Netflix went from investor darling to strategic screw up destined to fail because of hubris and incompetence.

Netflix’s major risks were (and still are) content exhaustion driven by media owners launching their own streaming services or, potentially, a glut of streaming services fracturing the market. Netflix started developing (and buying) its own content to protect against this and so far this has worked out. Netflix has even managed to weather the storm presented by Disney+ and it looks increasingly like a handful of services will dominate and the rest will struggle - the same pattern we saw with PCs, mobile devices, and auto manufacturers. (My own view is that Netflix was not as easy to spot.)

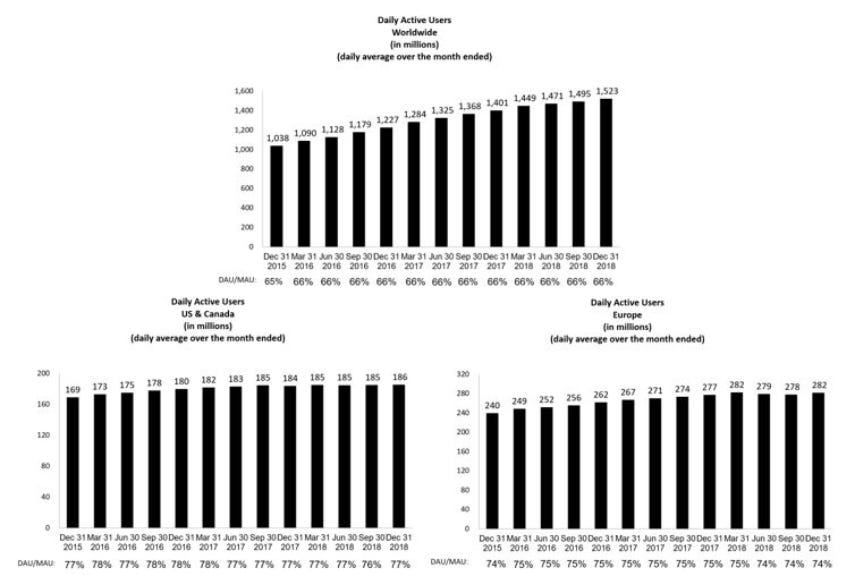

In the case of Facebook it was the Cambridge Analytica scandal which sent shockwaves through the world and gave birth to the #deleteFacebook movement. The stock plunged 40% in a few months, yet underneath, Facebook was still growing apace.

If we look at the DAU chart we can not detect the “disastrous 2nd quarter” or the substantial impact on Facebook’s growth. Of course, it could always be in the future, but once a company is dominant and the disruption cycle has become more iterative it’s much more likely to continue than during the period of massive innovation.

Investors must learn to ignore sensational headlines and instead focus on the underlying business fundamentals and behavioral changes at scale.

A major risk to Facebook was the switch from “PC” to “mobile” use. Facebook began its life primarily as a PC centric “website.” Had it not successfully transitioned to mobile, separated its messenger app and made key acquisitions (WhatsApp[2014] and Instagram [2012]) it likely would have struggled. By the end of 2018 all of this was well in the past. Facebook’s current risks playing out in the media are around regulatory risk due to misinformation abuse, the ongoing “#deletefacebook” voices, its fight with Apple over tracking technology, relevance to younger audiences, and how much growth it can still manage. These are more incremental risks than the ones faced early on in the disruption cycle.

What if it never goes down?

Some businesses stay “expensive” for years, sometimes decades; and this approach will cause us to “miss out” on them. While true, I find it entirely acceptable; as the primary goal is to avoid permanent loss of capital (i.e. buying Blackberry). It is possible to simultaneously avoid predicting the winners of early disruption and still benefit from large growth runways if we are patient in our behavior and rational in our analysis.

Looking forward, there are a number of industries today where we see disruption without a clear winner. AI, VR/AR, Genomics, EVs and the surrounding renewable energy industry are areas like this. The rise of various “fin-tech” platforms is also in this group.

Slightly less unknown is the disruption in the music/audio streaming industry. It now seems reasonably clear that Spotify and Tencent Music are going to be winners and grow for quite some time (in both cases we have seen competitors leave the battlefield and changes are becoming more incremental; yet the potential growth is still substantial). Unsurprisingly, both are not available for a “cheap” price today - and they may never be. But it is also entirely possible that Spotify commits a Netflix or Facebook like mistake, sending its market value plunging while its underlying business remains in tact.

In the area of remote meetings, Zoom seems like it may emerge as a long term winner - but I would argue it is still a bit early since we haven’t seen companies like Google, Facebook, Microsoft, etc. surrender yet - in fact they appear to be gearing up for battle. If/when we see competitors ceding the battle and disruption making way for iterative change, the future is likely somewhat more predictable as far as who will “win.” As with autos, it is perhaps “obvious” that online meetings will replace traditional meetings and this area will grow massively. Far less obvious at this stage, is who the winners will be or what the business economics will look like.

Time will tell.

For these newer industries, I believe the best thing to do is nothing. Wait until a clear winner emerges (if they ever do) and in the mean time watch from a distance. Headlines will be full of investors who got rich by picking the correct winner early; and if you can play that game, that’s great for you. But we must balance these headlines against the unwritten headlines about the hoards of investors who picked the wrong horse: the investors in Commodore, Blackberry, and any of the thousands of failed auto companies.

We are possibly better off avoiding the temptation of trying to predict winners in early disruptive environments and instead wait until its much more obvious who the winners are. Then wait until they stumble.