Looking back at: Groupon

Confusing a backward looking narrative with a forward looking prediction is one of the worst errors investors make. We tend use our skills at crafting historical narrative as a proxy for future prognostication.

This is ultimately a problem of availability bias.

Not only do we know today what happened; but the noise that made predictions at the time difficult is largely absent from our field of study.

The best way to train ourselves against this is to look back at businesses that didn’t succeed (or didn’t succeed as much as expected) in a way that approximates what we would have known at the time, without the benefit of hindsight. This forces us to ask the questions “could we have known at the time that this business was headed for stagnation or destruction.” Given that MOST businesses are headed for an unpleasant destination, we should assume that the new, exciting businesses we love today are going to end up disappointing us rather than that we have correctly picked the tiny amount of wheat from the acres of chaff.

Let’s look at Groupon.

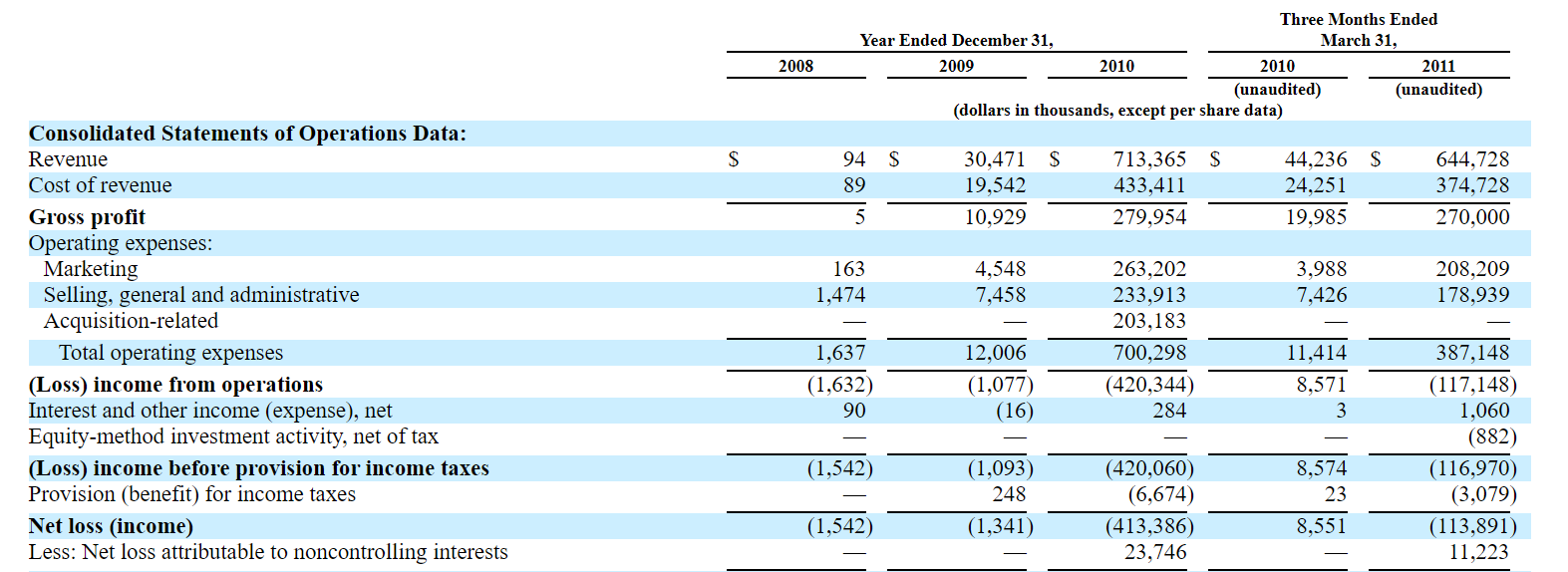

WAAAAYYYY back in 2011, Groupon filed it’s S-1 as it prepared to be a listed public company. Some of the key numbers are as follows:

3rd Quarter 2009 Sales: $3.3m

1st Quarter 2011 Sales: $644.7m

2009: 5 North American Markets

2011: 175 North American Markets and 43 Countries

2009: 152,203 Subscribers (43,014 customers purchased in Q2 2009)

2011: 15,803,995 Subscribers (no comparable stat given)

2009: 116,231 Groupons sold in 2nd Quarter

2011: 28.1m Groupons sold in 2nd Quarter

2009: 37 Employees

2011: 7,107 Employees

That is a lot of growth; and the potential opportunity (“TAM”) is vast. To understand this, we need to think about Groupon’s position in the value chain and the inflection that it presented, provided as follows from the S-1

”Groupon is a local e-commerce marketplace that connects merchants to consumers by offering goods and services at a discount. Traditionally, local merchants have tried to reach consumers and generate sales through a variety of methods, including the yellow pages, direct mail, newspaper, radio, television and online advertisements, promotions and the occasional guy dancing on a street corner in a gorilla suit. By bringing the brick and mortar world of local commerce onto the internet, Groupon is creating a new way for local merchants to attract customers and sell goods and services. We provide consumers with savings and help them discover what to do, eat, see and buy in the places where they live and work.”

Groupon’s growth relies on two critical factors. The first inverts the cost/risk problem for merchants. Normally merchants pay up front to reach a certain number of customers (e.g. printing 10,000 coupons and paying a newspaper to print them, or send them via direct mail, etc.). Groupon’s pitch is “we will send it to 10,000 people for free and you only pay us if a lot of them actually buy something at a discount.” This presents virtually no risk for the merchant. The second is that it points the “global” internet canon at the “local” business. The promise of internet commerce was largely “your little shop can now reach the world.” Groupon’s pitch was “you can use the power of the internet to target all your potential local customers.” A free way for small businesses on a tight budget to quickly reach local customers? Who wouldn’t love that.

On the customer side, the proposition is equally compelling. Instead of randomly looking through the yellow pages or being bombarded with ads, Groupon provides me with relevant deals available at a discount if enough people like me sign up for them. Perfect.

Groupon also benefits from economies of scale and brand recognition. Once subscribers have a “habit” of using Groupon, they are unlikely to use something else. This causes the merchants to become reliant on Groupon. Customer use feeds merchant participation which fuels customer growth - the so-called “fly-wheel.” While this is expensive to set in motion (Groupon lost $x in 2011), once scaled it can become highly profitable and difficult to compete with (comparable to Amazon). At scale, a low margin business with highly efficient operations and customer habits is nearly impossible to compete with (Costco, Walmart, Amazon). In “social media",” once a habit is formed and associated with a brand it is nearly impossible for disruptors to take market share (Facebook, Google, etc). But spinning the flywheel is not as easy as it sounds.

Groupon is originally an “asset light” business. Unlike wholesalers or retailers, it does not have to store massive amounts of merchandise hoping it can sell it. It simply connects sellers to buyers and takes a cut from the transaction (this has changed over time as Groupon seeks to return to growth). This business model scales across products and services and requires no specialized knowledge. To sweeten the pie, if a deal doesn’t succeed, it does not cost Groupon much. Accumulated data allows Groupon to get better and better at knowing what prices customers would be willing to pay, which businesses are best and what customers desire - furthering its competitive advantage similar to companies like Amazon.

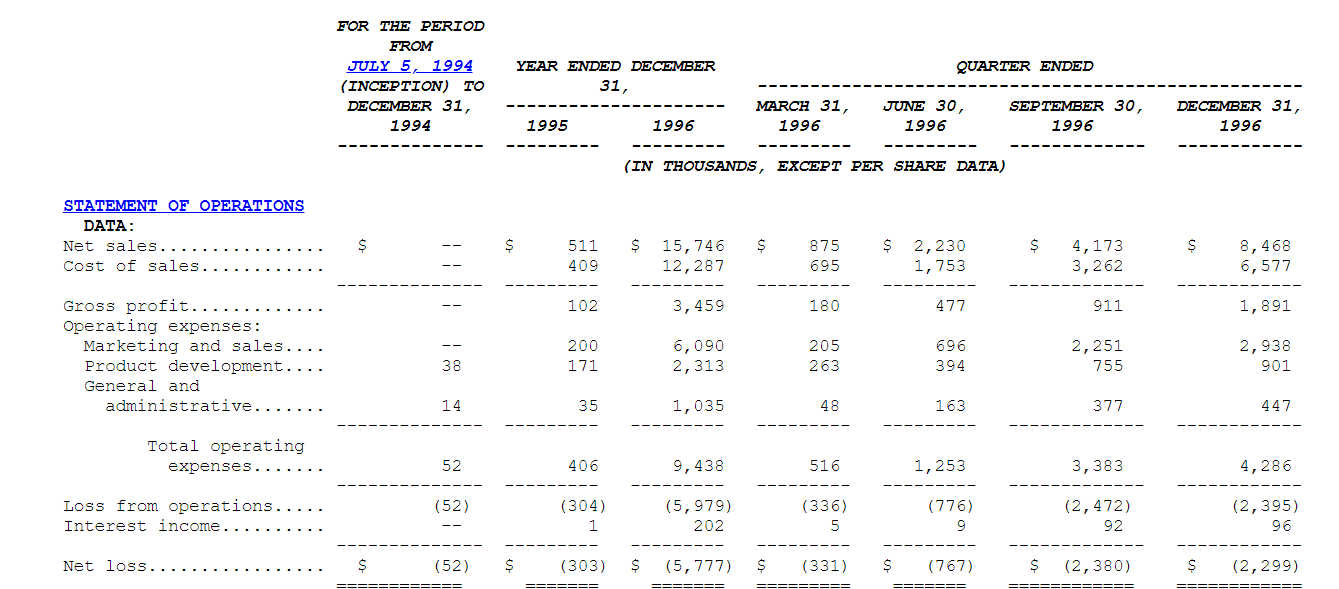

Let’s quickly compare the income statements presented in the S-1s of Groupon and Amazon.

Like early Amazon, early Groupon has dramatic increases in sales, and reasonable gross profits; but is pouring money into sales and marketing (and product development); deliberately delaying current profitability into the future. It makes little sense for a company with rapidly growing revenue and scaling its business to focus on being profitable - that comes later.

For the Groupon IPO investor, Amazon was a reasonable comparison and, in fact, potentially had an advantage by not building complex and expensive logistic services which, at the time, may have appeared as a liability. In hindsight, we can more clearly see that Amazon’s dominance in logistics now serves as an advantage. At IPO time, Amazon was also positioned as an “online book store” whereas Groupon’s prospects were much broader. At the time of Groupon’s IPO it was clear that online group purchasing was going to continue be a thriving industry; thus it was reasonable to believe that Groupon could go on to grow and dominate over time.

By the end of 2011, Groupon’s Market Cap was just over $14 billion giving it a Price to Sales ratio of 4.5, Gross Profit of 83% and 1.1B in cash. By the end of 2012, Revenue had grown from 1.6B to 2.3B, Gross Profits were 70% and the company had achieved positive operating income and reduced it’s net margin loss to 2.3%.

But Groupon shareholders had a different experience as signs of trouble began to emerge.

After reaching nearly $500/share in early 2012, by the end of that year shares were trading at $105. Groupon’s earnings were reporting a slowing (and potential contraction) in the core business and questions around it’s internal controls drove negative sentiment regarding the future of the company. Investors at the time had to decide if this was a “temporary problem” or a sign of “permanent loss of capital.” After all, even though the original business growth was slowing (or perhaps reversing) this could be a pivot to a new source of revenue. Amazon was not destined to just sell books; it reinvented itself several times and this was the way that high growth internet companies were supposed to behave.

Sure enough by the end of 2013, shares were back up to $250. Granted, the stock had not nearly recovered to its high, but things were certainly looking up. Having ousted it’s “quirky CEO,” the resumption of growth and the success of a new business type (goods) helped provide investors with some comfort. Nevertheless, healthy skepticism remained. International sales had fallen 24% and average spending was flat at $138/customer.

After reporting 2013 earnings in February of 2014, negative volatility took over. A write up in Forbes captures the sentiment perfectly:

Imagine it's Christmas morning and under the tree you find the shoes you have been eying for months. You are overjoyed, but when you try them on you realize the shoes are far too small and can't be returned. That is probably what it felt like to be a Groupon investor after earnings Thursday.

…

Despite strong revenue growth, the digital deals company still finished the quarter in the red, with a $81.2 million net loss thanks in part to a $85.5 million non-operating loss related to an investment in China and $34.5 million in acquisition costs. Including the China loss and acquisition costs the company reported a per share loss of 12 cents. Wall Street expected a GAAP loss of a penny. However, excluding the China loss and other costs the company reported 4 cents in earnings per share, beating a 2 cent earnings estimate. 1

By May of that year, shares had fallen to $110 forcing investors, once again, to decide if these were temporary setbacks for a company with a great future; or foreshadows of a more permanent decline. They did not have to wait long for some bright spots to emerge on the horizon.

Groupon acquired SnapSave and launched Snap later that year. This would allow them to extend further into general e-commerce and speed up the swelling growth of mobile attention.

Nor was this mere smoke and mirrors. The company posted $925m in Q4 sales that year, beating analyst expectations and its own guidance. Unfortunately, its future guidance did not impress. The year continued to go from bad to worse. Groupon would go on to lay off 1,100 employees and shut down operations in 6 countries. It also replaced it’s CEO with a former Amazon exec and its former head of marketing. This neither impressed investors nor did it alter the growth trajectory of the company.

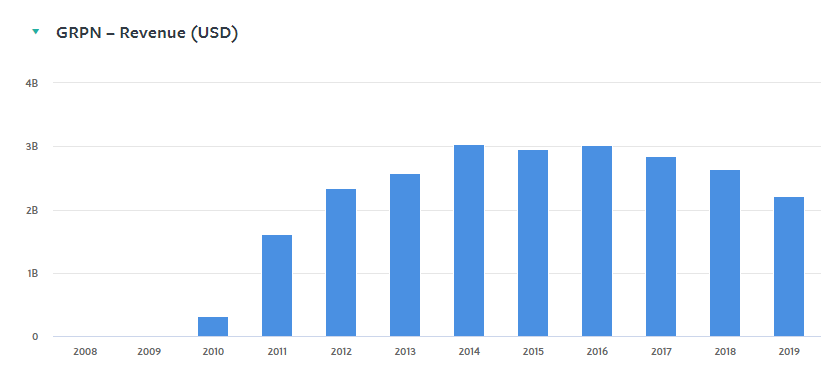

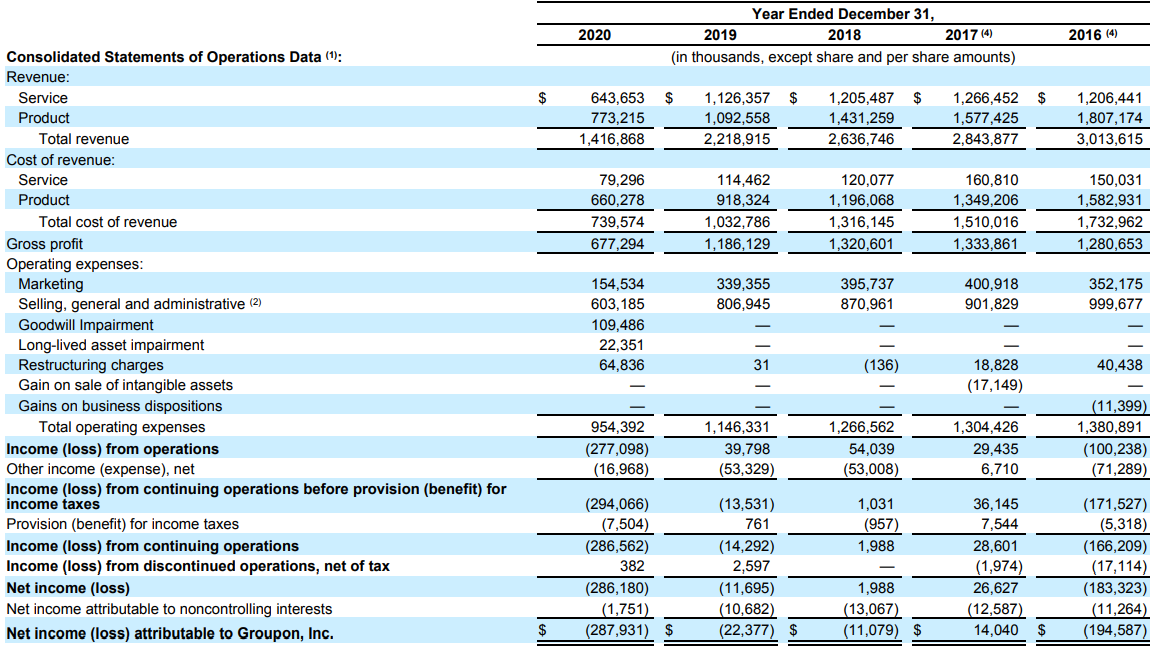

Groupon’s revenue has continued to decline (though fairly moderately):

while share price has had a similar direction, but in a less gentle way.

2020 aside, Groupon has been a fairly stable business:

It has worked diligently to try and maintain its existing business while finding the next inflection point.

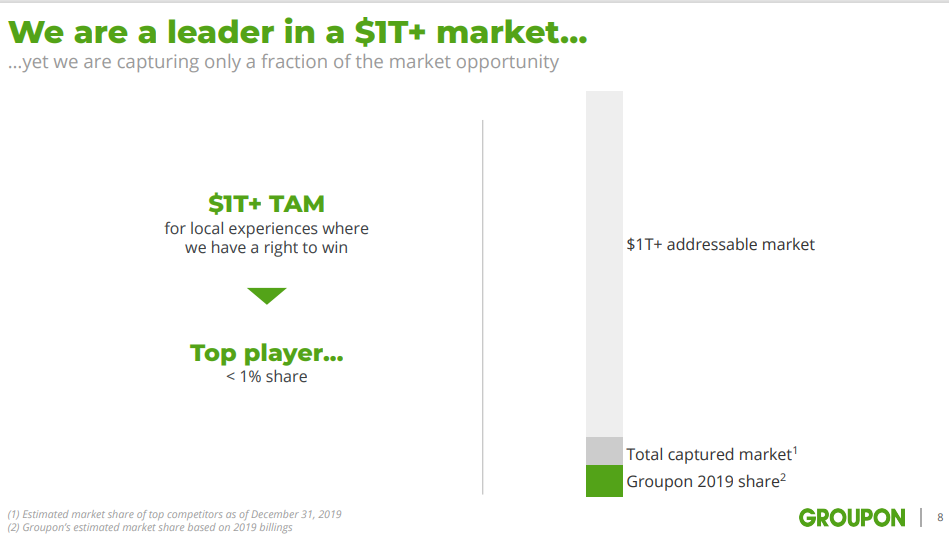

In 2021, Groupon is still the leader in the “fragmented $1T+ local market” and is still focused on connecting local businesses to local buyers - not an entirely improbable strategy. From it’s 2020 Q4 earnings release investor presentation:

Nevertheless, from IPO to date, investor returns compounded annually at -20.31%. From the first substantial fall (buying shares in Sept, 2012) investor returns were a less gut wrenching -5.6% CAGR. From Jan, 2016, -3.4% and for investors who chose the Mar 2020 pandemic, returns have been a very healthy 79% - despite a disastrous 2020 for the company.

Groupon was not an fantastical business with no prospects or high uncertainty. It was a well established, high growth, solid brand prior to its IPO; and it continued to grow for years after.

I do not want to paint the picture that Groupon is a “bad company.” To do so would be to admit that the wild swings in investor sentiment and expectations determine underlying business performance. Running a successful business is incredibly hard and capitalism is unforgiving and brutal. Groupon is still around and is still taking shots. Its employees still work hard, are intelligent and are tasked with substantial challenges in a rapidly changing environment. Its leaders must make difficult strategic decisions with unknown outcomes. It could STILL go on to grow massively, stagnate or shrink into oblivion.

The dominant narrative for Groupon’s "stall in growth is that the group buying-coupon industry got oversaturated and customers “burned out.” LivingSocial has a similar story attached to it. This may be true, but it is a backward looking narrative. It would have been difficult to determine at IPO time what the final growth curve would look like. Moreover, it is impossible to know that if Groupon, LivingSocial or other similar businesses would have had a different outcome had they made different choices. A challenge in any new business area is that the size, profitability, customer behaviors and so on are largely unknowable.

Consider, for example, today the “virtual meeting” business’ future is largely unknowable. We can not know how big it will be, how fast it will grow, how user behaviors will trend, how profitable it can become or which company will “win.” The long term economics, winners and losers in Electric Vehicles, Telemedicine, Augmented Reality, and a host of other businesses lay firmly in the future.

This presents a difficult dilemma for investors. A good way to reduce risk is to pay a low price. At a low price, Groupon would not have been a “bad investment” - in fact it could have been a great investment; while even at a “high price” Amazon proved to be an incredible investment. However, companies with favorable prospects based on recent high performance are usually not available for a low price. Thus it is far more likely to pay for an Amazon and get a Groupon than not. Since we tend to brag about our winners and “forget” our losers, the aggregate result is to make the business of investing in the future look much easier than it really is.

The future Amazon, Google, and Microsoft are laying the groundwork required for decades of unimaginable growth. Their Groupon-like peers are simultaneously, though unknowingly, laying the groundwork for years of stagnation and disappointment - if not outright destruction. Distinguishing one from the other remains a challenging prospect to be done with appropriate trepidation and respect for the past.

“Groupon Stock Takes A Wild Ride After Revenue Beat, Earnings Disappointment,” Forbes, Feb 20, 2014